Featured insight

Who Finances Central Asia's Strategic Autonomy?

Strategic autonomy in Central Asia is usually discussed with reference to transport corridors, critical minerals or high-level summitry. Beneath all of it, however, lies a question of capital, and the capital is not the region’s own. The Eurasian Development Bank estimated in June that the region needs at least $251 billion in investment by 2030, $170 billion of it in energy, far beyond what the region can raise itself. The projects meant to reduce the region’s inherited dependencies must be financed by someone else. This has a consequence that is easy to miss: external influence over Central Asia now shows less in the map of infrastructure projects than in the financing mix behind them.

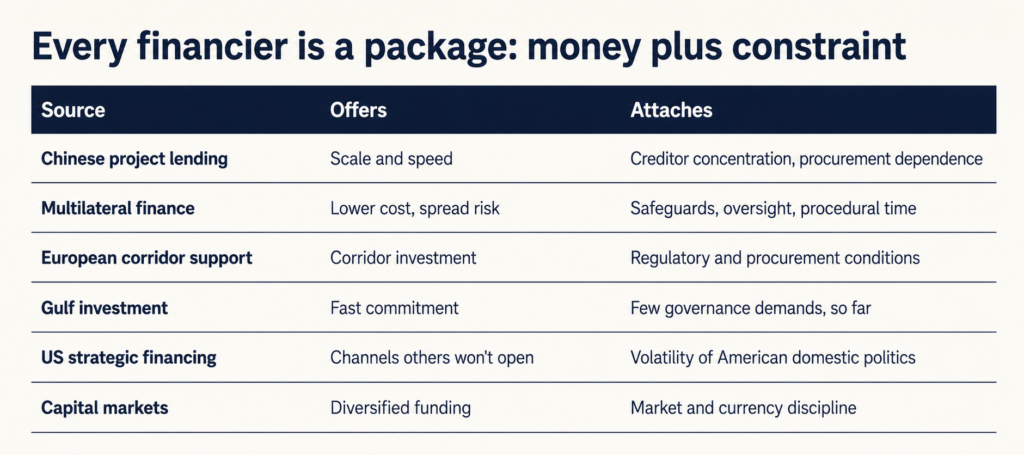

Each source of capital carries its own terms. Chinese project lending is fast and large, and it concentrates creditors and procurement in one country’s hands. Multilateral money is cheaper and spreads risk but it arrives with safeguards and oversight. Rogun has now shown both faces of that package, with the World Bank freezing financing in 2025 until Dushanbe produced a financing strategy and dam-safety protocols. European corridor support brings regulatory conditions. Gulf investment commits faster and asks less about governance. Financing linked to US strategic priorities opens channels no one else will, and imports the volatility of American domestic politics into the transaction. Borrowing on capital markets trades policy conditions for market and currency discipline. Each is money plus constraint, and choosing a financier means choosing which constraint to live with.

July shows the region assembling these packages in earnest, with Kazakhstan building the widest spread. The state railway, Kazakhstan Temir Zholy, filed for a Hong Kong IPO targeting about $1 billion, with proceeds earmarked for a new rail link to China: the instrument of diversification financing deeper connectivity with the largest existing creditor. A panda-bond issue is in preparation, and Masdar’s $1.4 billion wind project broke ground in late June. The Karachaganak processing plant is now contracted to Korea’s Hyundai Engineering at about $6 billion for construction through 2030. The field’s international shareholders refused to invest on terms Astana could accept, so the state, through QazaqGaz, carries the bill; how it will be financed has not been announced. Uzbekistan combines its established Chinese investment base with new American trade access and a financial-centre architecture designed for investors it does not yet have (Signal 4).

The paradigm pair is Rogun and CKU. Tajikistan has placed its defining project inside a multilateral framework whose conditions demonstrably bind but whose grants cover a fraction of the remaining bill. Kyrgyzstan is financing its share of the railway through sovereign borrowing and Chinese project credit, with far lighter external conditionality. Both are buying the same thing, externally financed autonomy, with different mixes of scrutiny and debt.

The intuitive reading of all this activity is that diversification dilutes dependence: six lenders constrain a government less than one. In practice, obligations do not cancel each other out; they add up. A government that owes procurement openness to the World Bank, debt service to Chinese policy banks and disclosure to foreign investors has multiplied the audiences it cannot afford to displease. Displeasure rarely blocks anything outright; it arrives as slower disbursement, costlier borrowing, or doors that quietly close. Diversification improves bargaining power at the moment of signing. It narrows discretion afterwards, because each new channel adds conditions without retiring the old ones. The region’s governments are becoming more autonomous in whom they can approach, and less autonomous in what they can subsequently refuse.

The test for the region’s governments is practical: keep procurement open across competing lenders, keep debt service within fiscal capacity, finish what they have started, and end up in control of the assets built with other people’s money. For the lenders, the test is the mirror image, and it connects to this issue’s opening essay. Capital is entering states that are settling their politics for the long horizon, and lenders will be tempted to read that consolidation as creditworthiness. The stability on offer, though, is the stability of authority, not of rules. The financial enclaves multiplying across the region (Signal 4) are that bargain made institutional: predictable rules for investors inside the fence, discretion outside it. And July showed the discretion runs both ways, with the World Bank’s Board declining its own Inspection Panel’s recommended investigation while approving new Rogun money. Neither side of these bargains is rule-bound all the way down. When the accumulated obligations eventually compete with one another, they will be renegotiated, not adjudicated, and which constraint a government honours first will be decided politically. Autonomy financed by others is autonomy on conditions, and the conditions are accumulating lender by lender.

From the July 2026 Target Trajectory Monitor. Full issue and subscription: target-research.org/ttm